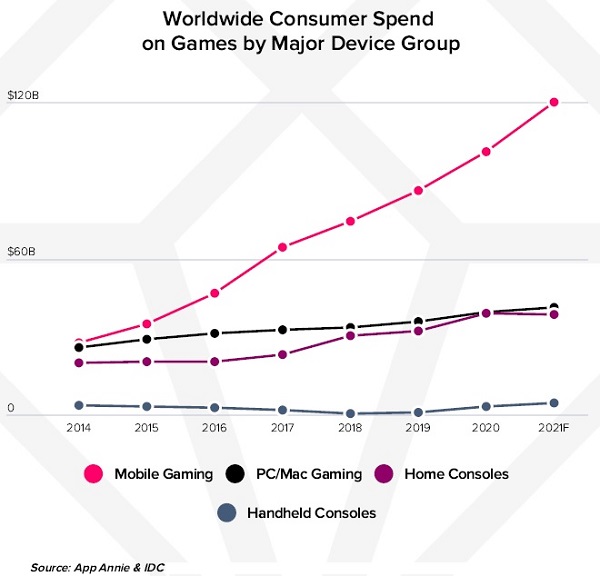

Worldwide consumer spend on mobile gaming will surpass USD 120 billion in 2021. This would be an almost 19% upsurge from last year, and evolution of almost 40% from 2019. At least, this is one of the most important indicators presented by ‘2021 Mobile Gaming Tear Down. Key Trends on Subgenres, Monetization & User Acquisition’, a key report from App Annie, a mobile market estimate service provider.

The growth of mobile gaming is impressive, but it’s even more eye-opening to see how it compares to other gaming channels, with 3.1x consumer spend on home game consoles in 2021. The console and mobile experiences are merging. Mobile devices are now capable of offering console-like graphics and gameplay experiences along with cross-platform competitive and social gaming features. The gaming market at large will benefit from increased engagement.

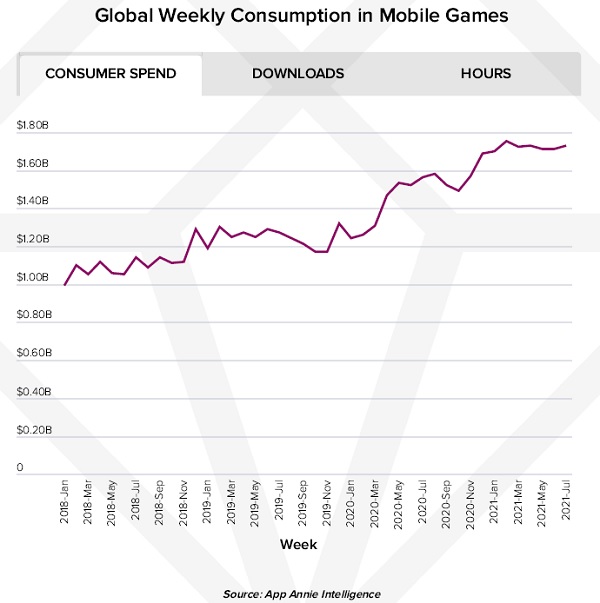

According to this study, one year into the COVID-19 pandemic, demand for mobile gaming has remained strong, with no sign of slowing down. Weekly downloads first surpassed 1 billion in March 2020, and have remained at that level since. In the first half of 2021, consumers spent USD 1.7 billion on both iOS and Google Play purchases per week in mobile games globally, up 40% from pre-pandemic levels. New gamers and existing gamers present unprecedented opportunities for growth.

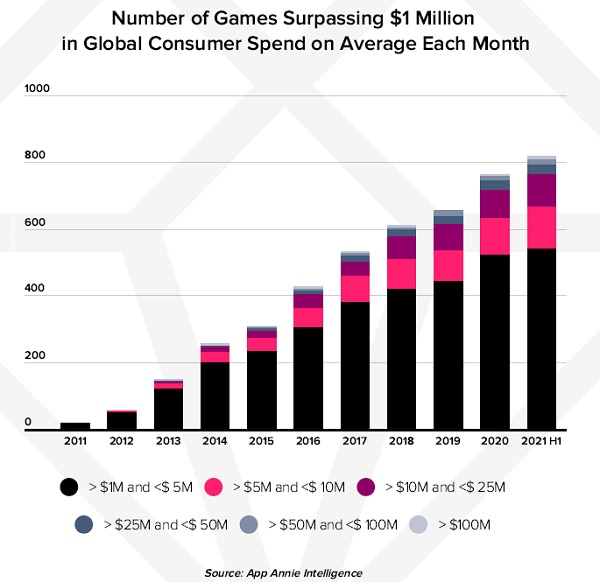

Consumers migrated more of their digital games consumption onto mobile in 2021. In H1 2021, there are over 810 games surpassing USD 1 million in consumers spend each month on average, with 7 of them surpassing USD 100 million. This was up 25% from 2019 at 650 games over USD 1 million and only 2 over USD 100 million, both in monthly spend. Improved connectivity, screen size and hardware have made it easier than ever before to enjoy premium gaming experiences on-the-go.

U.S., A TOP MOBILE GAMING MARKET

Across the world, mobile game adoption is surging, especially among emerging markets. Countries such as Brazil, Indonesia and Russia present a ripe opportunity for local and foreign mobile game publishers and investors. They are poised for stellar growth in the coming years. However, large, traditional markets are still leading the way.

While India is the world’s biggest mobile game market by downloads, United States tops mobile games market by app store consumer spend. Asia-Pacific (APAC) remained the world’s biggest region for consumer spend in mobile games (accounting for over 45% of market share), but that increase in market share has leveled, as other regions have caught up, led by the U.S., Germany and UK.

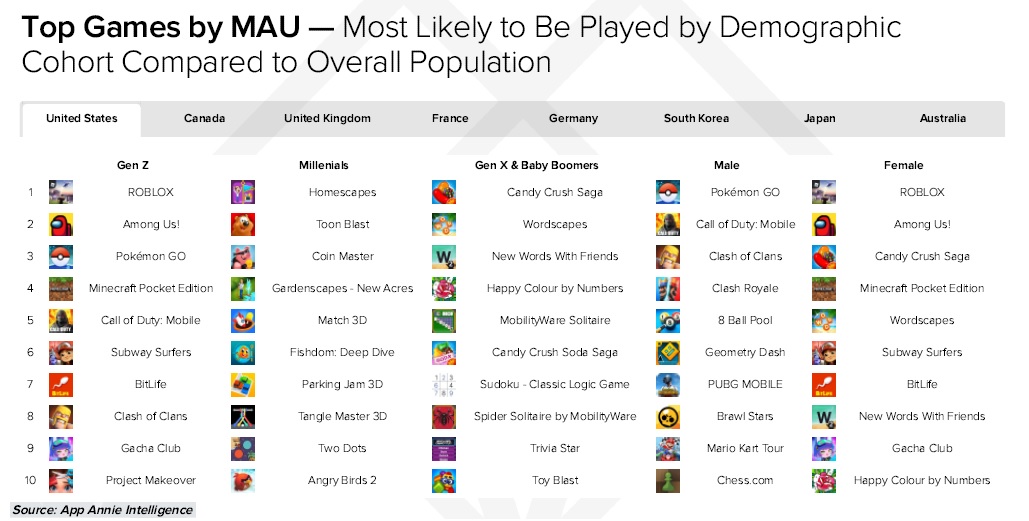

MOST ATTRACTIVE TITLES

Understanding demographics segmentation can help companies build out marketing campaigns and partnerships for games with demographics that match their target audience. In this sense, Roblox and Among Us! were clear favorites among younger demographics (Gen Z) globally, while popular Match 3 Games such as Candy Crush and Homescapes perform better among Millennials and Gen X/ Baby Boomers. Among Us! and Roblox also have higher tendency to be played by female audiences. Pokémon GO has enjoyed widespread popularity globally, but tends to skew towards a male audience.

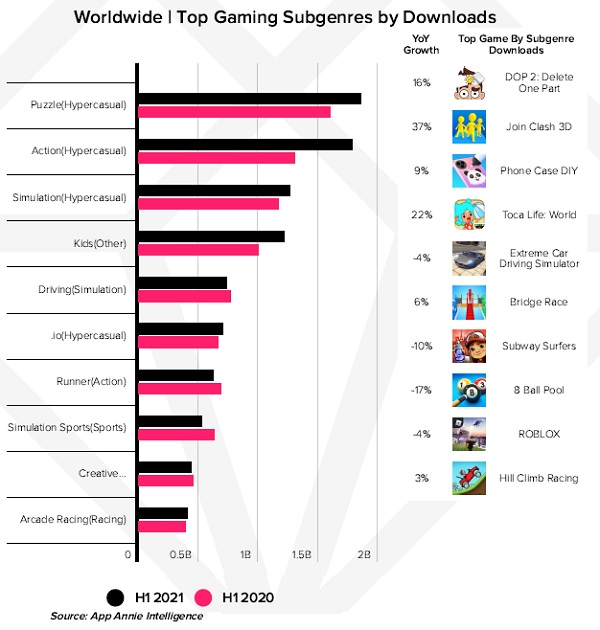

Hypercasual games were responsible for one-third of mobile game downloads in H1 2021, reaching 6.8 billion downloads, 2x more than 2 years prior and nearly 5x more than 3 years prior. Battle Royale, Shooters and MOBA Action subgenres were a key driver of time spent. RPG and Strategy games drove nearly 50% of consumers spend worldwide. These core genres have found success on mobile, proof of mobile’s ability to compete with console and PC for screen time.

Among the top 10 subgenres by downloads, 4 belong to the Hypercasual genre. Top Hypercasual game publishers produced a high percentage of hit titles, with over half exceeding 5 million downloads during H1 2021. The Puzzle (Hypercasual) subgenre had the largest single market share of downloads, while the Action subgenre has the highest growth year-over-year of 37%. Belonging to the Action (Hypercasual) subgenre, Join Clash 3D was the most downloaded Hypercasual game in H1 2021. Other high-growth subgenres were catered for Kids, such as Toca Life World, which reached the #1 rank among the Education category on iOS in over 100 countries.

FUTURE TRENDS

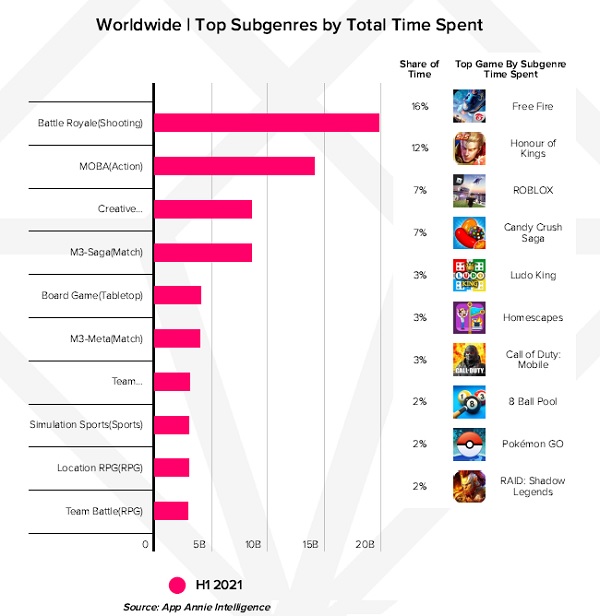

Core games drove 50% of time spent share, led by action genres. Games under Shooting, Action, RPG and Strategy genres made up around half of total time spent in games globally in H1 2021. The top 3 subgenres by market share of time spent rely heavily on social and online features. Free Fire is a standout game among Battle Royale (Shooting) games, a subgenre commanding 1 of every 4 minutes spent in games globally. Social and online features help cultivate deeper play and foster longer retention. It is expected that games with these features will drive usage as mobile gaming continues to captivate the world.

Top Shooter games offer robust monetization pathways ranging from battle passes to gacha/loot boxes to cosmetics. Layering gameplay tags on top of market performance metrics across a peer group can give a deep and specific knowledge into what is driving success for a game.

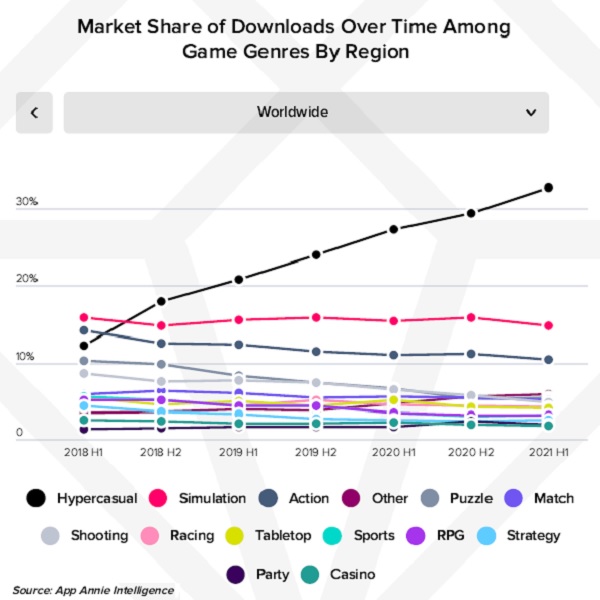

Looking ahead, App Annie mentions three future trends to consider: 1) Hypercasual games will continue to drive the market share of downloads in most regions; 2) Innovative genres are poised to disrupt incumbent market dominance, and 3) Shooters, action & genres with online and social features will further drive global gaming time.

As mobile gaming continues to grow, there will be more publishers expanding to new genres and markets, and consumer preferences will continue to shift. What was true in 2020 may not apply in 2022, and publishers need to monitor the market trends carefully to stay competitive and increase profits.