By Damian Martinez, journalist at G&M News.

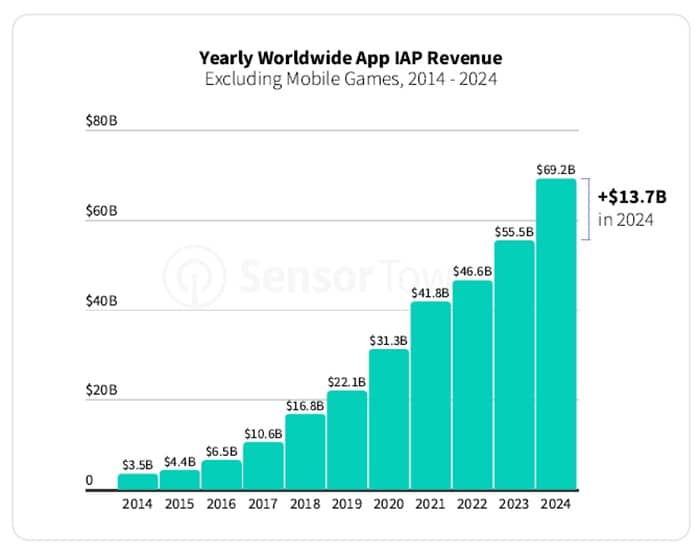

We are witnessing a mature mobile market. Growth in time spent on mobile devices is slowing, while revenue continues to soar. Mobile applications (apps) have consumers’ attention; now they are monetizing it. In 2024, revenue from in-app purchases (IAP) and subscriptions continued its rapid growth, up 13% year-over-year (YoY) globally to USD 150 billion, according to the State of Mobile 2025 report developed by Sensor Tower.

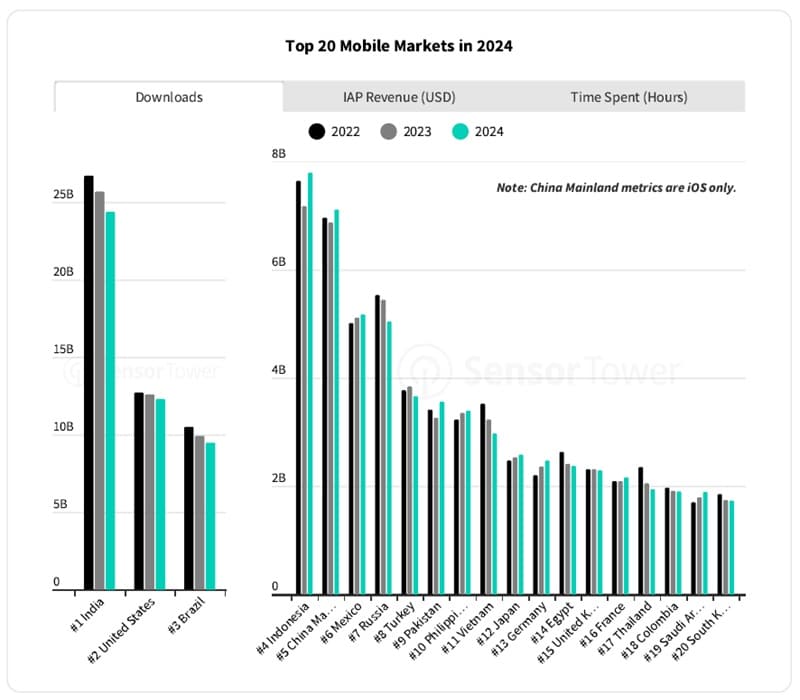

This included particularly strong growth in top markets in North America and Europe. The United States (U.S.) led the way with USD 52 billion in consumer spend. With game revenue growth lagging from non-games, some gaming-focused markets in Asia experienced more modest growth or even slight declines YoY.

What has helped create this revenue boom on mobile? Consumers are spending more time than ever on their mobile devices and are becoming increasingly comfortable making purchases on them. Time spent climbed in most markets, though it has leveled out in a few like the U.S. and Japan. Meanwhile, downloads declined for the fourth straight year. Half of the top 10 markets still achieved positive YoY growth, including Indonesia, China Mainland, and Mexico.

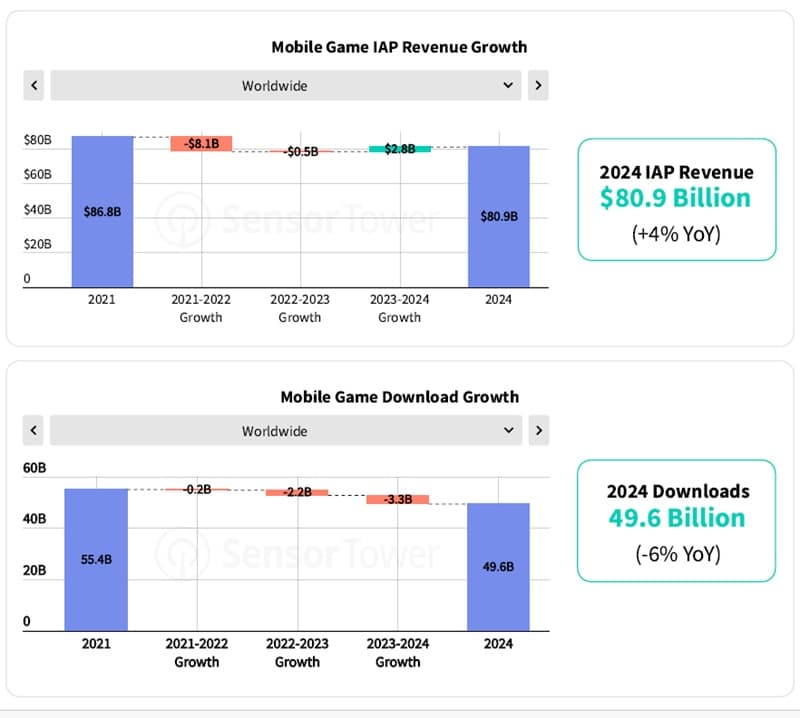

Mobile gaming bounced back with positive year-over-year IAP revenue growth for the first time since 2021. However, the landscape has changed over the past few years, with Strategy and Puzzle driving growth while RPG continued to decline. Mobile game IAP revenue rose to USD 80.9 billion in 2024, up 4% YoY, even as downloads declined by 6% to USD 49.6 billion. This fall reflects markets stabilization amid industry consolidation and broader tech sector pressures.

Despite this, consumers are spending more time on mobile devices and increasingly making purchases, driven by improved gaming experiences and enhanced monetization strategies. Emerging markets like Mexico, India, and Thailand fueled much of the growth, with spending rising 21%, 17%, and 16%, respectively. Turkey led with a 28% increase, while Saudi Arabia posted a 14% rise. Established markets such as the U.S. and EMEAR regions saw steady growth, while North Asia faced headwinds, with Japan experiencing a 7% drop due to economic and currency challenges.

While most markets saw a decline in downloads, regions like Indonesia and Saudi Arabia provided bright spots of growth. Looking ahead to 2025, consumer spending is expected to climb further as developers prioritize retention and high-quality gaming experiences.

Global weekly mobile game spending surpasses 1.54 billion dollars in 2024

Developing markets are increasingly important to the global mobile gaming economy, with spending and engagement steadily rising. Seasonal spikes vary by region: in the U.S., downloads and revenue peak during year-end holidays, while September sees the lowest downloads. In Japan, summer drives strong performance for downloads and revenue. Understanding these regional patterns is vital for developers aiming to maximize engagement and revenue in a competitive market.

In 2024, Strategy games topped global consumer spending with 17.5 billion, closely followed by RPGs at 16.8 billion. Puzzle and Casino genres secured third and fourth positions, contributing 12.2 billion and 11.7 billion, respectively, with Puzzle games showcasing robust monetization despite declining downloads. Action, Simulation, and Shooter genres recorded significant growth, with Action leading the way in revenue gains (+46%). Sports games, though facing a drop in downloads, still generated 2.7 billion. These trends underline the strong monetization potential of competitive and immersive genres such as Strategy, RPG, and Action, which continue to captivate players globally.

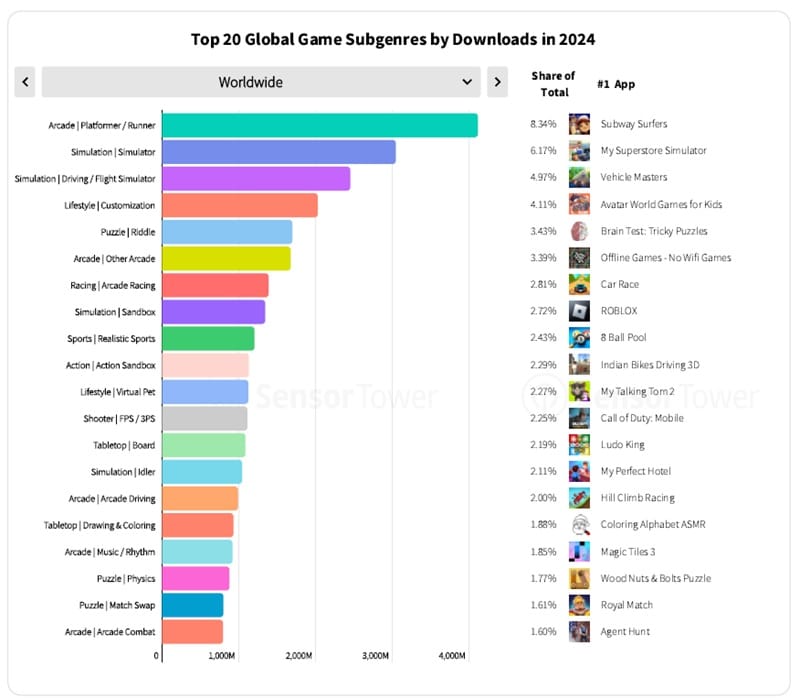

In 2024, Strategy games dominated global consumer spending, with 4X Strategy leading the charge, capturing just under 10% of the market share, driven by Last War: Survival. Match Swap Puzzle games followed closely at 8.67%, fueled by the success of titles like Royal Match. RPG subgenres, including Squad RPGs (6.14%) and MMORPGs (5.59%), continued to deliver strong contributions, showcasing their lasting appeal among dedicated players.

Casino Slots (5.37%) and Coin Looters (5.14%) demonstrated robust monetization, while Battle Royale games, led by Game for Peace (3.05%), maintained a loyal player base. Simulation subgenres, particularly Tycoon/Crafting, also gained momentum. These trends highlight the dominance of immersive and strategy-focused genres, with a balance of enduring favorites and new entrants driving sustained growth in the market.

A notable shift towards core genres

The number of new mobile game releases among the top 1,000 in the U.S. has steadily declined since 2020, dropping from more than 200 to just above 100 in 2024. Despite this reduction, average downloads per game have remained stable at 1–2 million, highlighting a shift toward quality over quantity. Mid-core and core titles, including Shooters like Call of Duty: Warzone Mobile and MOBA newcomer Squad Busters, have seen strong adoption. Meanwhile, enduring hits such as Roblox and Subway Surfers continue to deliver significant download volumes. Additionally, Strategy and Lifestyle games are gaining momentum, creating new opportunities for innovation in niche categories.

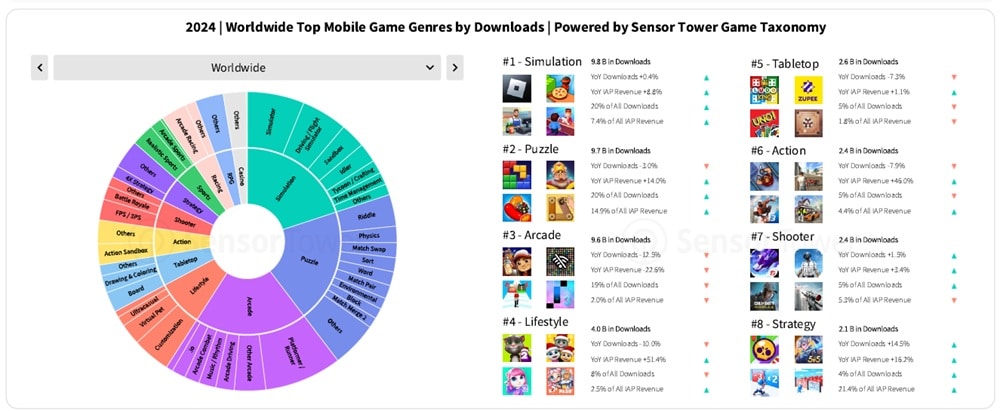

Arcade Platformer/Runner games led global mobile game downloads in 2024, capturing 8.34% of the share, driven by the enduring popularity of Subway Surfers. Simulation subgenres followed closely, with Simulator (6.17%) and Driving/Flight Simulator (4.98%) reflecting strong interest in immersive, task-based gameplay exemplified by My Supermarket Simulator 3D and Vehicle Masters. Lifestyle Customization titles, led by Avatar World, gained traction, showcasing the growing appeal of personalization.

Puzzle Riddle games, including Brain Test: Tricky Puzzles, maintained a steady 3.43% share. Meanwhile, Shooters such as Call of Duty: Mobile held competitive positions, underscoring sustained demand for action-packed experiences. The diverse performance across genres highlights a balanced demand for casual and immersive games, offering developers opportunities to innovate and adapt to evolving global player preferences.

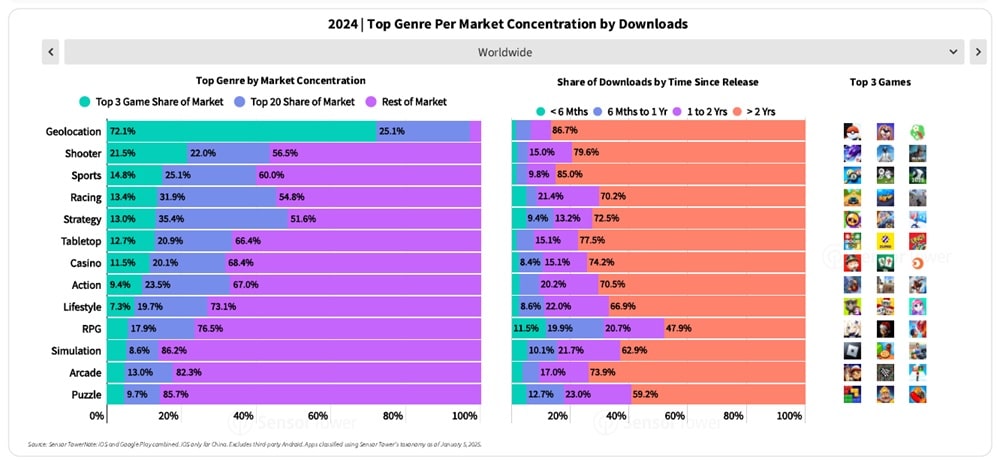

In 2024, Geolocation games exhibited the highest market concentration, with the top three titles accounting for 72.1% of downloads, significantly outpacing Shooter (21.5%) and Sports (14.8%), which faced broader competition. Meanwhile, Simulation, Arcade, and Puzzle genres remained highly fragmented, with more than 80% of downloads distributed across smaller games. Geolocation and Sports genres also leaned heavily on older titles. In contrast, RPG games saw less than 50% of downloads driven by older titles, highlighting the competitive momentum and appeal of newer releases.