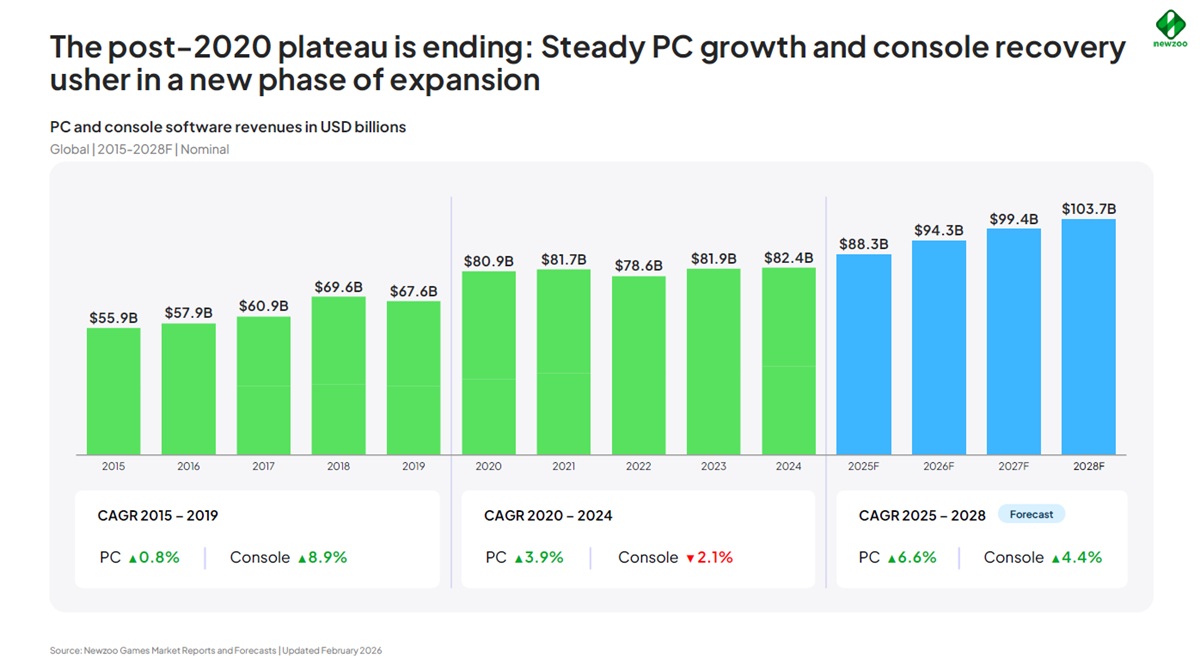

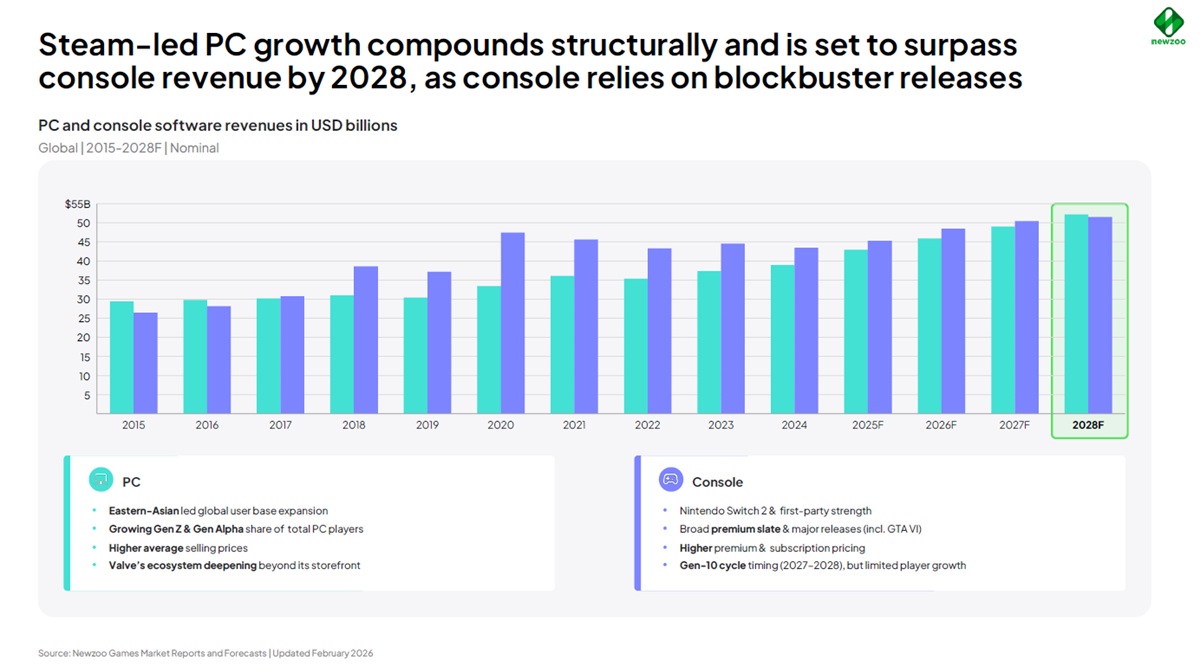

In its latest study, denominated PC & Console Gaming Report 2026, prominent market research company Newzoo projects PC revenue will surpass console revenue by 2028. PC is expected to grow at a 6.6% compound annual growth rate from 2025 to 2028, compared to 4.4% for console. Overall, the PC and console gaming market is projected to reach USD 103.7 billion by 2028. The combined revenue for these segments grew 7% year-over-year in 2025 to USD 88.3 billion, and forecasts it will reach USD 94.3 billion in 2026. This expansion was the first notable rise since the pandemic slowdown and the start of a more measured upsurge cycle expected to continue through 2028.

MONETIZATION TRENDS

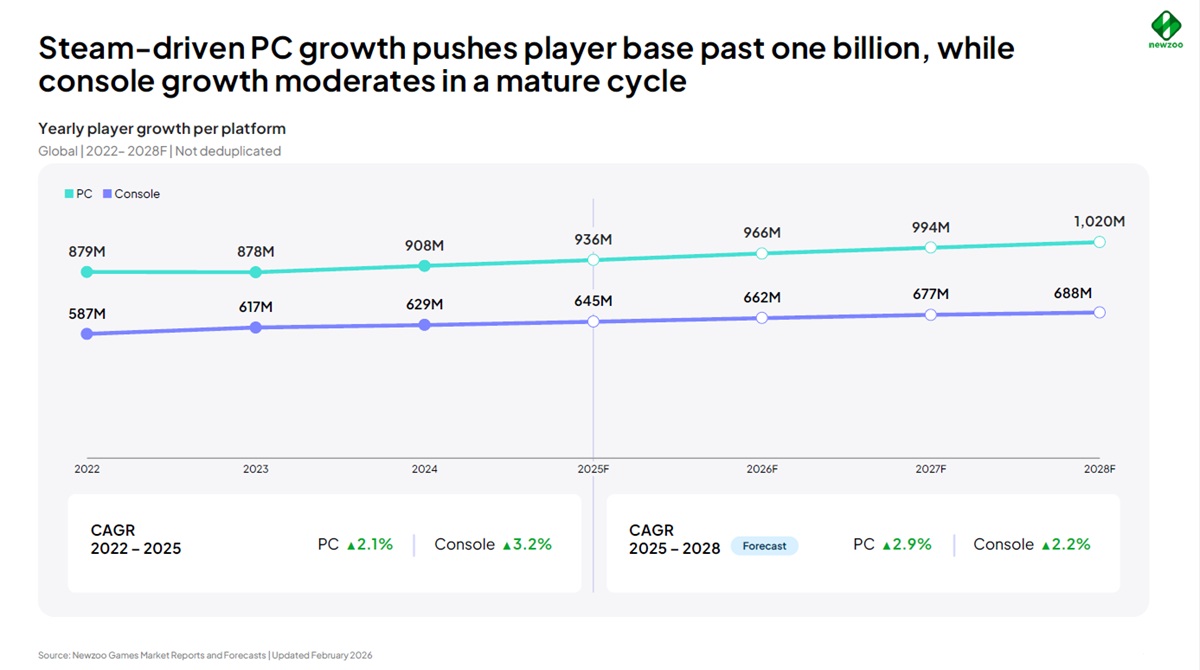

On PC, premium games represented 29% of total revenue and were the main growth driver, with an 11.8% increase across AAA, AA, and indie releases. PC monetization remains structurally microtransaction-led. In 2025, microtransactions accounted for 48% of PC revenue (USD 20.6 billion), while premium game sales represented 29% (USD 12.5 billion). Engagement outside the top 20 titles grew from 33% in 2022 to 42% in 2025. The player base is expected to exceed one billion in 2028, driven by regional expansion, especially in East Asia. For instance, China grew 11.7% YoY in 2025.

Regarding console, premium titles accounted for about half of revenues in 2025, a 12% year-over-year rise. Games priced above USD 50 comprised nearly 80% of premium revenue. Microtransaction revenue declined slightly, which reflects pressure across some live-service ecosystems. Subscription revenues grew modestly, driven mainly by price increases and tier upgrades. Console remains more dependent on blockbuster premium releases and hardware cycles. Mature markets such as North America and Japan continue to generate higher spend per player.

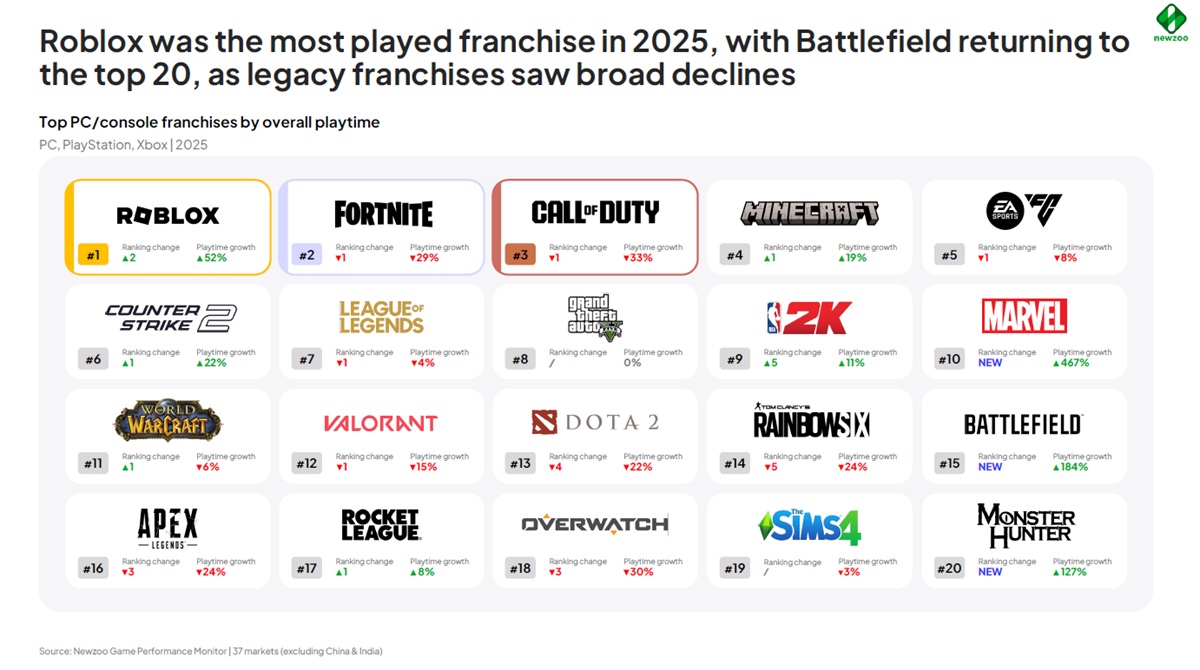

Across PC and console, Roblox was the most-played franchise last year with a 52% increase in playtime. Fortnite was second, followed by Call of Duty. Battlefield returned to the top 20, while legacy franchises saw broad declines. The list of the top 20 is completed by Minecraft, EA Sports FC, Counter-Strike 2, League of Legends, Grand Theft Auto V, NBA 2K, Marvel, World of Warcraft, Valorant, Dota 2, Rainbow Six, Battlefield, Apex Legends, Rocket League. Overwatch, The Sims 4, and Monster Hunter.

PLAYTIME LEVELS

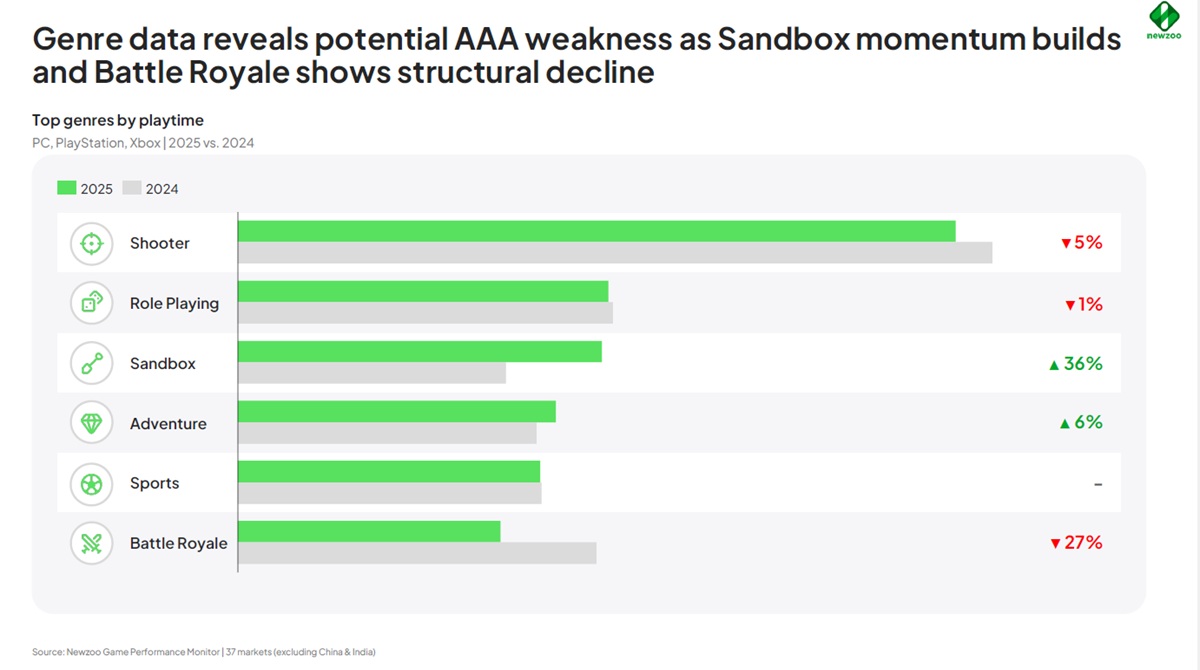

Overall playtime remained broadly stable in 2025 (-1% vs. 2024), reinforcing that growth is increasingly occurring through more effective monetization rather than expansion in global player time. At the same time, several traditionally dominant AAA genres (including Shooter, Battle Royale, and Sports) are seeing structural decline, with growth segments like Sandbox not fully absorbing lost hours. In fact, playtime for battle royales dropped 27% in 2025 compared to 2024, while shooters had a not insignificant 5% dip in 2025 compared to 2024. Sandbox games, however, saw a major increase in 2025, rising 35% in playtime compared to 2024, with a lot of that driven by the success of Roblox.

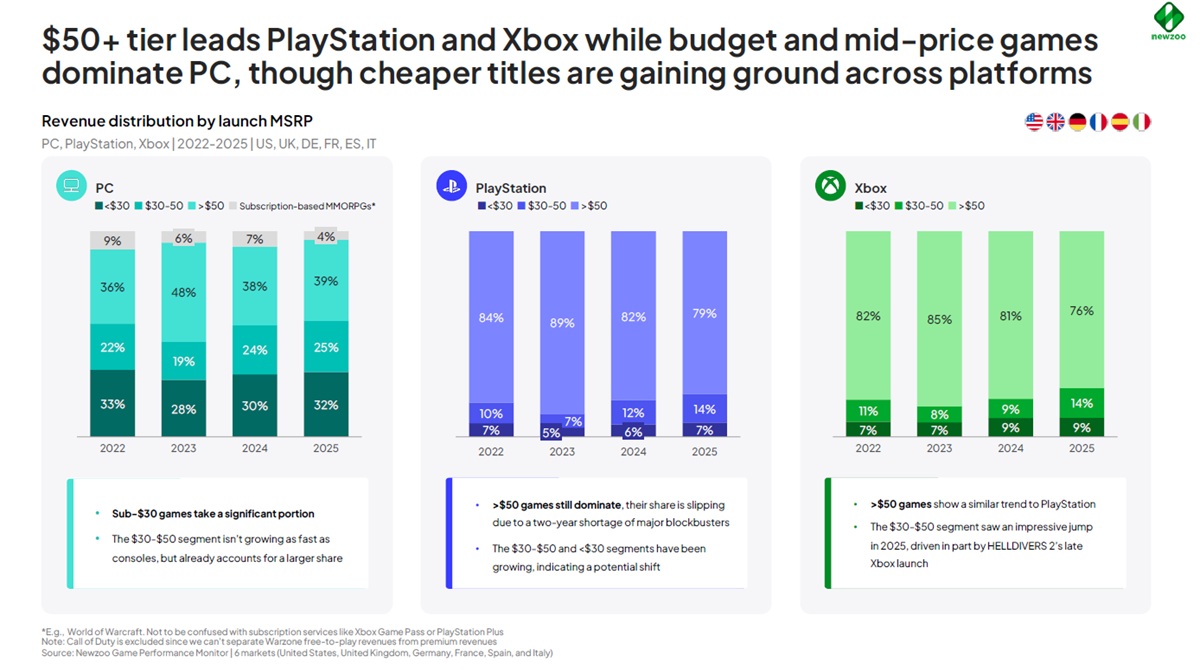

Elsewhere in the report, Newzoo analyzed changes in premium pricing dynamics. In major Western markets (the US, UK, Germany, France, Spain and Italy), premium spending increased in 2025 despite declines in playtime. The USD 30 to USD 50 price tier is emerging as the fastest-growing premium segment. On PC, titles under USD 30 are more popular, with 26 games in this market segment surpassing USD 5 million in revenue in 2025, compared to 17 in 2024. Newzoo found that titles above USD $50 remain most popular on console, though it is flattening on some platforms, including Xbox. On Xbox, Game Pass has enabled players to try different experiences with way less friction.

To sum up, the global PC and console gaming sector is expected to steadily progress in the upcoming years, despite AI-driven demand for high-end memory chips potentially elevating prices.